Is Pet Insurance a Smart Financial Decision for Pet Owners?

Insurance for pets is becoming more and more popular as the cost of veterinary care goes up. Pet medical expenses can vary from simple treatments to surgeries that save lives, which makes lots of pet owners think about whether should they put money into health insurance for their pets or not. Some people see it as a shield against sudden costs while others are doubting if the price paid for premiums is justifying possible advantages. This article looks at the things that affect if pet insurance is beneficial, by thinking about expenses, what it covers, and different financial plans.

The Growing Popularity of Pet Insurance

More people who have pets are seeing the worth of pet insurance for managing costs related to animal hospitals. In the year 2023, more than 5.6 million animals in America had this kind of protection, showing that a lot more people are getting these policies now. But still, most pets in America don't yet have such cover because many people aren't sure if it's worth their money or not.

The growth in pet insurance is propelled by increasing costs of veterinary and enhanced treatment alternatives that can prolong the life span of pets but they bring along substantial financial pressures. With more owners of pets looking at different choices, it becomes necessary to understand details related to pet insurance so a knowledgeable decision can be made.

The Cost of Pet Insurance vs. Veterinary Expenses

Insurance costs for pets change based on factors like the pet's breed, age, and health condition, along with how much the policy covers. A full accident and sickness cover generally costs about $676 per year for dogs and $383 for cats. If you only get a plan that covers accidents, premiums are cheaper, it can cost around $204 annually if you have a dog or about $116 if your pet is a cat. They have policies that include emergency treatments but they do not cover illnesses. Though these numbers might appear controllable, as pets grow older, the premiums rise with them too. Normally, more aged animals often bring about much higher expenses.

The expenses of a vet can also change based on what treatment is needed. Regular checkups, vaccinations, and small sicknesses might not require insurance costs because they are quite cheap. But serious conditions like cancer, injury, or chronic diseases can create medical bills that go up to thousands of dollars. For pet owners who do not have much savings for emergencies, insurance gives financial help when unexpected medical problems arise.

Coverage, Limitations, and Exclusions

Animal insurance usually pays for different kinds of health services, like operations, diagnostic checks, and medicine that a doctor gives you. But not every cost gets paid back to the person who has the insurance.

These policies have things called deductibles (which are amounts some people must pay before any payment from their policy can happen), percent of reimbursement (how much money they will get back), and limits to how much coverage is given per year, all these factors decide how much pet owners end up spending themselves. An 80% reimbursement policy with a $500 deductible, for instance, will take care of a large part of the expenses but still make pet owners accountable for starting costs.

Exceptions are very important in finding the worth of a policy. Many insurance companies don't cover conditions that already exist, this means pets who become sick with ongoing illnesses before they get insured won't receive aid for these treatments. Usually, preventive care like vaccinations, dental cleanings, and living arrangements (spaying or neutering) is not included unless you buy an extra plan dedicated to wellness. Understanding these exclusions helps pet owners assess whether insurance aligns with their financial expectations.

The Impact of Age and Breed on Premiums

The cost of health insurance for pets is mainly determined by their breed and age. Generally, younger animals have less expensive premiums because they are less prone to serious illnesses. But, when these pets get older, the cost related to keeping them insured goes up greatly. For example, a middle-size dog's monthly insurance could begin at approximately $35 when the dog is still young.

But it can go beyond $150 by the time they reach 12 years of age. Cats are generally less expensive to insure, but their pricing also shows the same pattern. The financial possibility of covering them for longer periods should be thought about because owners of pets might pay more in premium fees over a certain number of years than what they would need to spend on medical bills directly from their pocket.

Certain types of dogs also might have more expensive insurance because they are likely to develop some health issues according to their genes. Breeds that are big and can easily get hip dysplasia or heart disease, may need a policy that costs more compared to those small healthy dogs. In the same manner, purebred cats with past hereditary conditions could face higher premiums than mixed-breed ones. Factors like these must be considered when deciding if pet insurance is a cost-efficient solution.

Alternatives to Pet Insurance

If you are not sure about getting pet insurance, other financial plans can be a backup for vet costs. One of these is creating a special savings account just for your pet's health costs, which lets the money grow over time. This technique makes sure that you are ready in terms of finance but without having to pay premiums for protection that might go unused. But, if there is a sudden expensive emergency, maybe the money in a savings account will not be enough unless you have been putting funds for many years.

There are other choices too, like paying for veterinary care by installment plans provided by clinics or looking at charitable bodies that help pet owners who struggle financially. Also, some animal hospitals give discount schemes for regular care which lessen the necessity of insurance. Although these options provide flexibility, they cannot offer similar protection from unexpected and costly illnesses as what insurance can cover.

Weighing the Pros and Cons of Pet Insurance

Insurance for pets has its pros and cons which are dependent on an owner's economic condition and ability to endure risk. The main advantage is financial safety, making sure that high-cost treatments do not lead to tough choices about the care of a pet.

It also gives calmness, letting owners concentrate on their pet's health instead of how much medical procedures cost. However, the disadvantages are increasing insurance costs, possibly not using all benefits fully, and some policy restrictions that might not pay for every veterinary bill.

People who give high priority to financial security in times of unexpected health emergencies for their pets might find insurance a good option. This is particularly true if they have young and healthy animals. On the other hand, those with substantial savings or elderly pets having pre-existing conditions may see less advantage in ensuring their pets. It's important to consider your financial strength, chances of facing big medical bills, and other options available that can help decide if the need for pet insurance suits you as a pet owner.

Conclusion

To decide if the cost of pet insurance is justified, you need to deeply examine veterinary costs, prices for the insurance, and what it does not cover. Insurance can be very helpful in handling surprise medical bills but how effective it is depends on things like your pet's age, breed, and general health condition. Also there are other financial options available for taking care of a pet such as having savings accounts or financing plans set up specifically for this purpose. In the end, those who own pets must evaluate their financial readiness and potential dangers linked to vet expenses before reaching a knowledgeable conclusion about buying pet insurance.

Related Articles

How To Treat Myelodysplastic Syndromes: A Comprehensive Guide

By - Alison Perry

How to Treat Postural Orthostatic Tachycardia Syndrome: A Comprehensive Guide

By - Madison Evans

How Creative Names Can Make Vegetables Your New Favorite Food?

By - Noa Ensign

Valparaíso: A City of Colour and Chaos

By - Elena Davis

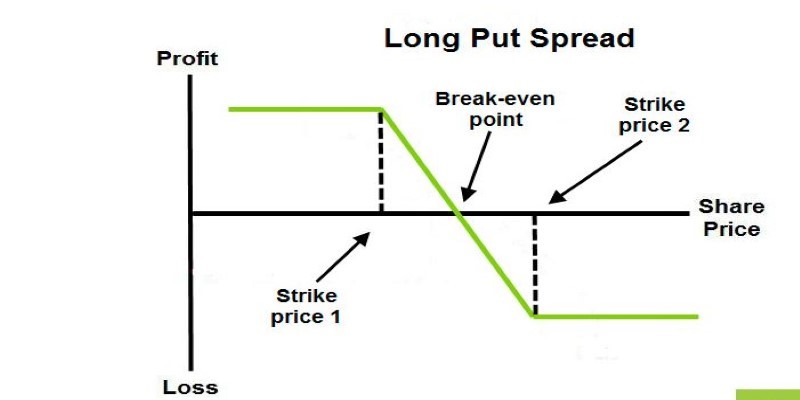

Mastering the Long Put Spread: A Smart Bearish Strategy

By - Sid Leonard

Mobile Devices and Young Children: What Parents Should Know and Do

By - Kristina Cappetta

Is a Few Minutes of Exercise a Day Enough to Prevent Hip Fractures

By - Korin Kashtan

Whispers of Ecuador: A Journey Through Land and Time

By - Paula Miller

10 Simple and Enjoyable Activities for Retirees to Stay Active

By - Aldrich Acheson

Comparing Personal Loans and Lines of Credit: Which Suits Your Financial Goals

By - Elva Flynn

Mallorca on a Budget: What to Expect in Terms of Costs

By - Juliana Daniel

10 Tips for Budgeting Around the Holidays Without Stress

By - Susan Kelly